Poker, Tax Politics, and the Byrd Rule

Everything, in the end, is Senate procedure

Readers: if you are here for shutdown content, you will have to wait until Friday. This is a piece I’ve been meaning to write for a while about a very specific provision of the One Big Beautiful Bill Act. It’s technical and if you don’t care about poker or tax minutiae or Senate procedure, it may not be worth your time. But I find it fascinating. -MG.

Dear Friends,

If you win money playing poker or betting on football in the United States, you owe ordinary income tax on it. That is, you add it to line 8b of Schedule 1 of your 1040 and it counts toward your total income for the tax year, no different than W-2 or 1099 income. You pay the man.

This is somewhat unusual globally—there are lots of different tax regimes, but many countries (including Canada) do not generally tax gambling winnings—but not out of character for the U.S., which tends to treat most sources of income as taxable.

The first question that comes up is what does it mean to win money? That sounds like an easy question, but it’s actually pretty tricky. If I win $50 playing poker in my basement on Friday night, that’s obviously $50 in winnings. But if I win another $50 on Saturday and lose $80 on Sunday, what exactly just happened?

For most people, common sense says they won $20 over the weekend. That’s certainly what they tell their buddy as the office on Monday. So they simply net their total wins and losses and call it a day. If they play poker 20 times in a year, they just add up their net winnings and report whatever net money they won.1

This is not how Uncle Sam thinks about your weekend of cardplaying. He thinks you had $100 in gambling winnings and $80 in gambling losses. For the IRS, each session was distinct event, because you realized the winnings when you got up from the table or cashed in your chips.2

Luckily, Uncle Sam does not make you pay taxes on the full $100—you have to report it as income on your tax return, but you can deduct the $80 in losses elsewhere on the tax return. So in the end you only end up paying taxes on the $20 in winnings. Seems fair, right?

It’s not. Well, if you are a professional gambler, it’s basically fair. The $100 can be treated as business income and the $80 as an expense, and the whole thing nets out on your Schedule C and by the time it hits line 8b of your Schedule 1 and then line 8 of the 1040, it just looks like $20 in income. No big deal. You even get the benefits of being self-employed—professional gamblers can take all the usual deductions for business-related expenses and whatnot.

But if you aren’t a professional gambler—whatever that means3—it actually becomes a non-trivial problem. For one, some states don’t allow the deduction of losses, meaning you could be on the hook for state taxes on the full $100 if you live in, say, North Carolina.4 More importantly, on your federal taxes, the winnings are reported as income toward your overall adjusted gross income (AGI), but the losses come as below-the-line deductions against your AGI.5

This means that you will ultimately only be taxed on the net winnings from the gambling, but the winnings themselves (before losses) will artificially inflate your AGI. That’s bad. If your net poker winnings were $20,000, but you got there by “winning” $300,000 and “losing” $280,000, all of a sudden your AGI looks $280,000 bigger than your actual income.

This could phase you out or completely disqualify you from things like the child tax credit, the Roth IRA deduction, the dependent care credit, and a host of other means-tested tax breaks. It can also increase your Medicare premiums and alter your social security benefits.

There are some interesting strategic cardplaying consequences to this. For example, if you win a big poker tournament for a large amount of money, you suddenly have a strong tax incentive to play a lot more tournaments for the remainder of the year, since all of the buy-ins for those tournaments are now tax-deductible against the big win. Depending on the size of the win and your other income, that could be a 30%+ discount if you are in the higher marginal tax brackets.

But the main upshot is that any poker player—winning or losing—who correctly files their taxes pays a penalty, at least relative to what common sense would say about winning and losing money in gambling endeavors.

Of course, poker players are nothing if not good at complaining, so all of this has been boilerplate grist for discussion at the tables and in the online forums for years.

Enter the Big Beautiful Bill, and Senate Procedure

When the One Big Beautiful Bill Act6 (OBBBA) passed, it contained a surprising provision aimed at gambling income.

Here it is, section 70114, in its entirety:

SEC. 70114. EXTENSION AND MODIFICATION OF LIMITATION ON WAGERING LOSSES.

(a) IN GENERAL.—Section 165 is amended by striking subsection (d) and inserting the following: ‘‘(d) WAGERING LOSSES.— ‘‘(1) IN GENERAL.—For purposes of losses from wagering transactions, the amount allowed as a deduction for any taxable year— ‘‘(A) shall be equal to 90 percent of the amount of such losses during such taxable year, and ‘‘(B) shall be allowed only to the extent of the gains from such transactions during such taxable year.

‘‘(2) SPECIAL RULE.—For purposes of paragraph (1), the term ‘losses from wagering transactions’ includes any deduction otherwise allowable under this chapter incurred in carrying on any wagering transaction.’’.

(b) EFFECTIVE DATE.—The amendment made by this section shall apply to taxable years beginning after December 31, 2025.

There are essentially two different things going on here:

Beginning in 2026, only 90% of gambling losses will be deductible; that’s the upshot of the first paragraph; and

The “special rule”—more on this in just a second—which was set to expire in 2026, is now permanent law.

Let’s talk about the second one first. The “special rule” was originally found in the 2017 Tax Cuts and Jobs Act,7 Section 11050:

SEC. 11050. LIMITATIONS ON WAGERING LOSSES

(a) In General.—Section 165(d) is amended by adding at the end the following: “For purposes of the preceding sentence, in the case of taxable years beginning after December 31, 2017, and before January 1, 2026, the term `losses from wagering transactions’ includes any deduction otherwise allowable under this chapter incurred in carrying on any wagering transaction.”

For purposes of completeness, here’s the original (pre-2017) section 165(d) from Title 26 of the U.S. Code that is being amended:

Losses from wagering transactions shall be allowed only to the extent of the gains from such transactions.

What’s going on here? Prior to the 2017 changes, professional gamblers were allowed to take deductions from non-wagering business expenses (hotels, travel, etc.) up to any amount, because the limitation on deductions only applied to losses from “wagering transactions”. The 2017 provision capped the total deduction (from losses related to wagering transactions and non-gambling business expenses) at the amount of gambling winnings.

The 2017 provision, however, was temporary, expiring at the end of tax year 2025. And so, circling back to the OBBBA, its provision in the second paragraph Section 70114(a) does nothing more than make the 2017 rule permanent. That is, the current status quo, which is worse than the pre-2017 rules for professional gamblers, will now be locked into place without expiration.

But functionally, nothing will be different in tax year 2026 from tax year 2025. The same rules apply. And the rule does not affect non-professional gamblers at all.

It’s a completely different story with the first paragraph of Section 70114(a). This is brand-new and may have a huge effect on a variety of gamblers, both professional and non-professional. By reducing the amount of losses that can be deducted to 90% of total losses, every winning gambler will have an increased tax burden, and even some losing gambler might pay taxes on their (non-existent) “winnings.”

Imagine a successful high-stakes tournament poker pro, with $1.4 million in earnings during the year, against $1.2 million in tournament buy-ins and business expenses. Prior to the BBB, that would net out to $200k in profit and a federal tax bill (assuming the 37% bracket) of $74k, for a post-tax income of $126k. Under the new law, only 90% of the $1.2m would be deductible, so net winnings would look like $320k, for a tax burden of $118k and a post-tax income of just 82k.

Now imagine a break-even non-professional gambler, with $100k in winnings and $100k in losses. That has the AGI problem, but the tax burden has traditionally net to zero, since 100% of the losses are deductible. But now only $90k can be deducted, resulting in a tax burden on $10k of income that literally doesn’t exist.

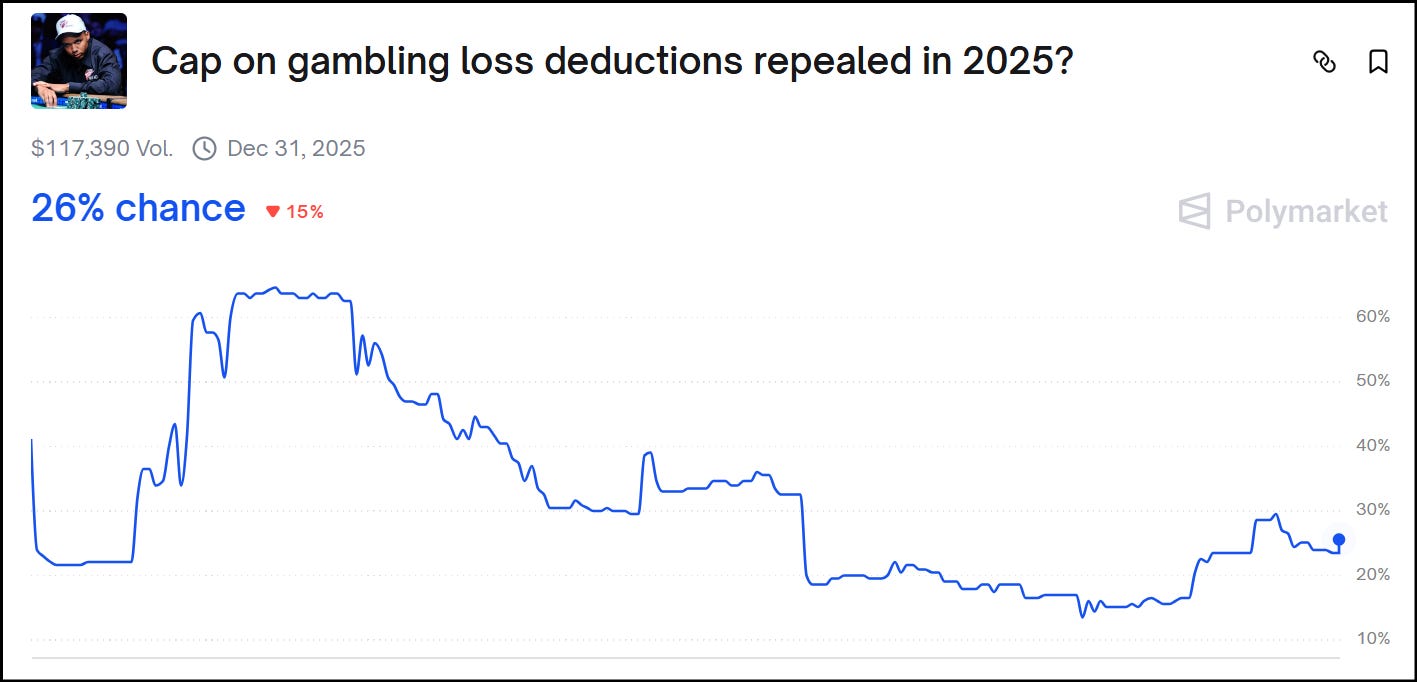

This did not go unnoticed in the poker world, or among anti-tax Members of Congress. But despite some late-breaking grassroots lobbying efforts and the opposition of some of the Nevada delegation, the provisions were not removed or adjusted in the final bill, and went into law on July 4, 2025.

Absent adjustment, they will take effect for the 2026 tax year. Several members of Congress have introduced legislative fixes since then, but none have gathered much steam on the Hill to date. Betting markets—ha!—currently have the chance of a fix this year as a 3-1 underdog.

Why did this happen?

There are basically three hypotheses for why anyone would want to make this change.

The first is that some important interest group wanted the substantive change. Let’s survey the stakeholders. We know the gamblers themselves hate it. What about casino operators? No, they dislike it too. It doesn’t gain them anything financially, and it could hurt overall gaming revenue and/or negatively impact tourism to Las Vegas or other gaming destinations. Anti-gambling interests might be a decent candidate, but the provision only really affects winning and break-even players, which means it misses the vast majority of recreational gamblers.8

The only interest that even makes a little sense is sportsbook operators. With the proliferation of online sports betting in the last decade, outfits like DraftKings and FanDuel have had to deal with an age-old problem well-known to the Vegas sports books: most bettors can’t beat the house edge at sports betting, but some sports bettors are sharp and—unlike basically any other casino games against the house—can realize an edge.

Ands the sharps who have that edge tend to try to bet big money. It doesn’t do any good as a sports book operator if 98% of your customers lose money, but the 2% that win are betting massive sums. So the online sports books already go to great lengths to try to limit the size of bets for sharp bettors, but it’s a cat and mouse game.

One obvious way to neutralize the sharp bettors would be to tax them out of profitability. Winning sports bettors are working on very thin margins—overcoming the house edge on a sports bet and having a 2-3% edge yourself is considered a huge success—and so those with an edge need to bet very high volumes. Losing 10% of deductible losses could turn a high percentage of otherwise-winning sports bettors unprofitable. And when they quit, it would leave only recreational losing bettors on the websites. That would be great for the operators.

The problem is there’s no evidence for this hypothesis. And it would only be great for an operator if they were exclusively a sportsbook operator; anyone interested in also having traditional casino games would be potentially damaging that source of revenue. And the online sports books are all in the casino game. So this sort of seems like a dead-end.

A second theory—one that I sort of fell back on in the midst of all this—is that this was somehow related to Senate reconciliation procedure. The OBBBA had a steep price tag, and in order to bring it fiscal line with both the terms of the reconciliation instructions and public opinion, every billion mattered. The 90% gambling loss deduction change was scored to raise $1.1B in revenue over ten years, relative to the baseline of the 100% deduction. So maybe some staffer on some Senate committee was looking at some menu of revenue-raising provisions, found this one, and threw it into the bill along with a bunch of other revenue-raisers.

The problem with this theory is that $1.1B is chump change. And even if revenue was the reason the provision got in the bill, that still doesn’t answer the question of how the provision got onto that menu of revenue-raisers. And unless it was some sort of responsible-budgeting watchdog group, that just brings us right back to the substantive question: who actually likes this provision?

The final theory—and one I think I now believe—is that this provision is a purely procedural maneuver. The two things to note are (1) the 90% provision wasn’t included in the original House version of the OBBBA; it was added in the Senate; but (2) the provision making permanent the cap on business-expense deductions for professional gamblers was included in the House version of the OBBBA.

The latter point was something I missed last summer in the midst of all this, but knowing it opens up an entire branch of the procedural-explanation tree: the Byrd rule, which requires that all measures in reconciliation bills be free of extraneous, non-budgetary provisions. The permanent extension of the 2017 cap on non-wagering business expense deductions for professional gamblers that was passed by the House (where there is no Byrd rule) may have been in danger of being considered non-budgetary, because it didn’t significantly affect revenue or spending.9

So if the deduction cap wasn’t going to pass the so-called Byrd bath conducted by the parliamentarian and the parties in the Senate prior to floor consideration of a reconciliation bill, one way to save it would be to otherwise alter section 165 in a way that was obviously budgetary. And presto! One obvious way to do that would be the 90% change, which would obviously score as raising revenue, against any baseline. It would also explain why the change had to be to specifically to section 165; the only way to save the extension of the deduction cap would be to make the specific provision have a budgetary impact.

I have no idea if this is correct, but it feels plausible to me. One argument against it is that the House provisions didn’t score as “negligible” by the Joint Committee on taxation—which would have been the kiss of death; instead, it did show a small amount of revenue over 5 years. I’m not well-versed enough in the truly byzantine precedents of the Byrd rule to say for sure what that means. Or, for that matter, how to think about this aspect of the Byrd rule with regard to the current policy baseline that Senate Budget adopted for the bill, which would almost certainly make the extension of the wagering cap score as zero.10

If you are knowledgeable enough about the Byrd rule to straighten me out at this level of detail, I’d love to hear from you.

Well, so what?

Beside the wild story of the provision itself, I think there are a bunch of important political takeaways from all this:

Stuff gets lost in bills all the time. Even after so many years on the Hill, it still shocks me when provisions get into bills that (1) no one really knows how or why they go there and (2) relevant stakeholders get caught completely flatfooted. That the gaming industry didn’t see this coming until it was too late seems almost impossible to me, except that it happens with surprising regularity.

Substance is written to conform to procedure. Sometimes we think of legislative procedure as something that strongly shapes whether a piece of legislation passes or not, but I think a lot of people miss that the procedure dictates what is actually written. Even at a very precise-level. “They are saying this doesn’t score—how could we change it so that it does?” Another good example of this is committee referral; bills are written all the time to purposefully steer them to one committee rather than another in the Senate, such that they will be received and considered by a more favorable audience.

Ostensibly small changes can have outsized implications. If you knew nothing about gambling, you might look at the 90% deduction, and then at the paltry amount of revenue it would raise (in comparison to both the size of the bill and the size of the gambling industry) and just decide that this was just not that big of a deal. But dig a little deeper and you can see that this could have literally a livelihood-level impact on a set of people, and absurd perverse outcomes for another set of people.

Cheers,

Matt

In reality, most people who win $20 playing cards don’t report anything to the IRS. I’m sure the vast majority of small-stakes gambling winnings—especially basement home game winnings—are never reported. And of those winnings that are reported, I’m guessing most people (incorrectly) use the common sense method of accounting, rather than the actual IRS method.

None of this is easy to define—if I play online poker for an hour, go each lunch, and come back and play more on a different website, how many sessions is that? Is playing blackjack and the switching to roulette with the same chips two different sessions? (Apparently, yes). Some of the distinctions are made because recordkeeping would be impossible—you can’t count every hand of poker as a different win or loss—but in the end, this is at some level just arbitrary.

It’s also not particularly well-defined by the IRS. Here’s a good example: I won a writing contest in 2023 and the prize included an automatic entry to a $25k poker tournament. I played the tournament, but did not cash. I never physically touched any currency, and I couldn’t have touched any currency if I tried. Did I win $25k and then lose $25k? Or was that just one session where I won $0?

The old joke is that a professional poker player is anyone at the table who doesn’t otherwise have a job. The IRS, of course, has a series of tests to determine the answer, but it basically comes down to “are you taking this seriously, keeping records, and trying to make a significant portion of your income doing it.”

Of course, there are also seven states (including Nevada) that do not have an income tax at all, so no state tax is owed on gambling winnings.

You also cannot deduct losses in excess of your winnings, or carry losses over from year-to-year to offset future winnings.

Technically, “An Act to provide for reconciliation pursuant to title II of H.Con.Res.14,” P.L. 119-2, July 4, 2025.

Technically, “An Act to provide for reconciliation pursuant to titles II and V of the concurrent resolution on the budget for fiscal year 2018” P.L. 119-2, December 22, 2017.

Most casino games offer no theoretical way to win long-term. The two major exceptions are poker (where you aren’t playing against the house) and sports betting (where sharp bettors may have better information than the sports books). But even in poker and sports betting, 90% or more of players are estimated to be losing money in the long run. A very small number of gamblers—called “advantage players”—can successfully profit long-term at other games (most famously blackjack), but the casinos frown on their methods, actively combat them, and make it miserably hard to succeed at.

What constitutes “non-budgetary” is an endless rabbit hole of arguments and advisory opinions of the parliamentarian and discussions between Senate staff. Go ahead and knock yourself out and take a look starting at page 642 of this document. I dare you.

Seriously, don’t ask. But do tell, if you know more than me. I still can’t figure out if the Byrd bath for individual provisions budgetary impact is intended to be conducted at the current law level even if Senate budget assumes a current policy baseline for net impact in out years.

I was told by a Congressional staffer that reason #2 (the reconciliation bill needed $1.1 billion more of revenue) was why it was added. Whether that's truthful or not, I have no idea. You're certainly a lot closer to Congress (literally and figuratively) than I am.

I do believe that this will be repealed. However, I have no idea **when** that will happen; bad tax legislation (e.g. amortization of R&D expenses) tends to stay in the law for years. Given that no stakeholder likes this, and this will **eventually** drastically hurt the new (mostly) sportsbetting companies, I put the chance of repeal within ten years at 99.99%. However, I believe the prediction market odds of about 25% by year-end are quite accurate.

Excellent piece, and I appreciate the distinctions between “pro” and non-pro gamblers.

I’ll politely suggest that your sample tax calculations under the new 90% rule aren’t accurate. The 37% marginal rate doesn’t apply until a single taxpayer earns (for the pro, has a profit) over $626k, and $1.5 million for a married pro. And that high rate doesn’t apply to the first dollars of income that the pro earns - those are taxed at 10-35% - on the fair assumption that a successful pro doesn’t have a day job or other income.

But to make the point that the 90% rule taxes phantom income, you’re on solid ground.